ING Groep: Why I like the stock

Banks in Europe are well positioned for a non-zero interest rate environment. Lower contributions to government funds and excess capital leads to an attractive risk-reward scenario.

Disclaimer: These are my ideas and not personal investment advice. I don’t know your financial situation. Do your due diligence and do not blindly follow an article on the internet.

ING Groep is the largest banking group in the Netherlands. Recent history has not been kind to the stock returns of ING and other European banks. I believe the situation that caused the poor returns for European banks has already fundamentally changed. I like the stock of ING Groep and other well-managed EU banks.

Explanation to an 11-year-old

Zero interest rates are a historic anomaly and were terrible for banks.

Contributions to crisis funds (SRF & DGS) will decline meaningfully during 2024.

Excess capital.

Buying companies with sustainable returns on equity above 10% below book value leads to attractive long-term returns.

Strengths & Risks: ING is good at gathering deposits

1. Zero interest rates and the effect on banks

The basic business description of a bank is lending money at a higher rate than is being paid on deposits. This becomes very difficult when interest rates approach.

In a more normal rate environment, governments lend at 4% and the savings rate at a bank account is 3%. This 1% spread is the bread and butter of banking. there are costs associated with delivering banking services and they are paid out of this spread.

The gradual increase in US interest rates starting in 2016 caused profits of US banks to increase significantly and stock prices to follow suit.

Europe was mired in low interest rates for a little longer, but last year interest rates finally left the zero bound. Bank stocks however have not moved in unison. This is because of fear about the corporate real estate market and the economy.

In my view though this re-rating is still likely to happen. Banks with sticky deposit franchises will benefit.

I am not arguing that interest will not decline again. This is the current expectation of the ECB for example. What I argue is this:

Declining interest rates do not matter (as long as the interest rates do not go below 1.5%). In contrast, modestly declining interest rates are better than continued fast increases in interest rates (that create trouble for companies refinancing, especially in the real estate sector).

Currently, Europe is still in a benign interest rate environment, compared to the US. Which is helping to prevent higher write-offs on loans.

2. Contributions to crisis funds (SRF & DGS)

After the GFC a lot of systems have been put into place to make sure governments in the future do not have to pay for bank bankruptcies. One of the measures was higher capital ratios. Another measure was the creation of certain funds. These funds need to be filled by the banks. The most important funds for ING are the Single Resolution Fund and various national Deposit Guarantee schemes.

a. The Single Resolution Fund (SRF)

The SRF is an emergency fund that can be called upon in times of crisis. It can be used to ensure the efficient application of resolution tools for resolving the failing banks, after other options, such as the bail-in tool, have been exhausted. The SRF ensures that the financial industry as a whole ensures the stabilization of the financial system. All banks across the 21 Banking Union countries must pay a fee annually by law to the SRF. These fees are called contributions. The fund means that taxpayers are not first in line to pump money into a bank, should extra funding be required, since EU law requires all banks to pay into the fund annually (https://www.srb.europa.eu/en/content/single-resolution-fund).

The target level of the SRF (1% of deposits) was achieved on 31 December 2023. From then onwards the fund only needs to be maintained at this level. This means that future contributions will be a lot lower going forward (except when major bank failures happen).

Contributions to the SRF by ING were 300 mln euro in 2023

b. Deposit Guarantee Scheme

Next to the SRF a lot of national governments also came up with their own regulation to protect deposits. These schemes differ between countries, but most have some sort of fund. For ING the DGS (Deposito Garantie Stelsel) of The Netherlands is the most important. This fund like many other European funds will be filled in 2024. Given the expected growth of deposits, the Central Bank of the Netherlands (DNB) expects still some contributions dependent on deposit growth, but a significant drop in total contributions is in the cards.

Together this will lead to a combined decrease in regulatory cost of 400 mln euros

Governments seeing this drop in regulatory costs might increase bank taxes further. While unfair we have seen a lot of additional bank taxes in recent years. This ultimately harms users of credit and creates an unfair playing field. Just to not be too optimistic I estimate that bank taxes increase 100 mln euros for a combined total benefit of 300 mln euros for shareholders long term. In 2024 the benefit will be roughly 100 mln.

With a record profit of 7.3B, the lower costs of SRF and DGS will increase profits by 4.1% in the long term (enough to increase the dividend by 0.7%).

ING gives little attention to this. Possibly to avoid scrutiny from government officials.

3. Excess capital

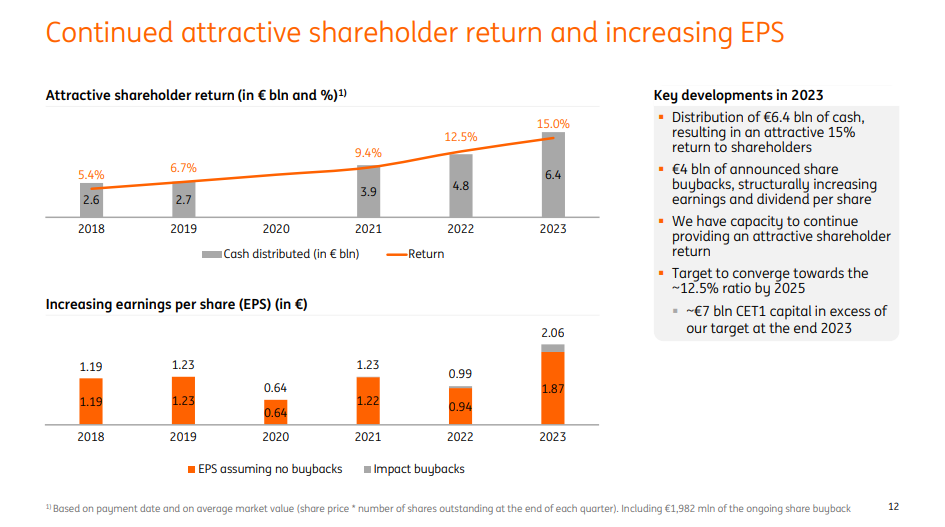

ING believes the bank is currently over-capitalized with a CET1 ratio of 14.7%. This is significantly above the target of 12.5%. ING Groep has been saying this for a while, but due to increased profits, the CET1 ratio increased last year from 14.5% to 14.7%. ING said during the presentation that it will again propose a new distribution at the annual meeting. Given the increased levels of capital, some additional distribution is likely in my opinion. While I don’t think this is a huge issue. Having some additional cash as a bank might not be such a bad idea. The excess capital still amounts to 7B euros. If ING would be able to return this to shareholders this means a one-time dividend of 16.7% on top of the regular dividend. The most likely scenario is sticking with the payout ratio and a higher share buyback program.

Especially given the inclusion of this slide which clearly shows the impact of buybacks on earnings per share.

4. Buying companies with sustainable returns on equity above 10% below book value leads to attractive long-term returns.

Kind of obvious.

ING delivered a 14.8% return on equity in 2023 and aims for 12% going forward. Equity is 52B euros and market cap 44B. I think 12% is a reasonable target (challenging with the current CET1 capital ratio of 14.7%, but achievable with the target CET1 ratio of 12.5%). Given that 12% is above 10% and 44B is below 52B I think the potential return is attractive. The company has clear potential to trade above book value especially when the environment becomes more favorable to banks.

If ING delivers an 11% return on equity and the company trades at book value I roughly double my investment in 5 years.

5. Strengths & Risks of ING Groep

In investing I think too much attention is given to demand growth and not enough to supply dynamics.

The Great Financial Crisis and the zero interest rate policy afterwards have created significant consolidation in certain European financial markets.

This is also true for the Netherlands. With Fortis disappearing the market is served by three large banks. ING, Rabobank and ABN AMRO. There are some new financial upstarts and some small struggling banks (SNS), but in my view, this competitive landscape is ripe for at least economic rewards on capital.

If you look at ING it is 2/3 retail and 1/3 wholesale banking. Retail is split roughly evenly between the Netherlands and the rest.

Returns are great in The Netherlands retail and Germany and decent in the other divisions.

Strengths

ING historically has been very good at gathering deposits. Given that interest rates are above zero this skill becomes valuable again.

In addition to this ING has strong digital capabilities for a bank. The best example of this is Germany. This is a competitive market with many banks. ING Groep however manages to get great returns without an expensive bank branch network.

Risks

Supposedly safe lending. ING says it lends money to low-risk clients. Historically however the bank made mistakes investing in gathered deposits. The best example of this was the supposedly safe US derivatives that ING invested the US gathered deposits in.

In lending as in investing, I tend to prefer a barbell approach. With very safe and risky investments. In lending this would mean more short-term German and Dutch government bonds, more consumer lending, and more SMB loans.

To make room for this lending I would love them cutting back their position in mortgages. Potentially ING could still make the mortgages, but sell them for a fee to investors who like return-free risk (pension funds come to mind like pension funds).

Especially in Australia with 36b of mortgages, I have my doubts and the risk and return profile (Australian banks are fairly expensive at the moment, so maybe this is a good opportunity).

Conclusion

Bank returns in Europe have been bad, but that bad decade has come from a very specific economic environment. Returns going forward for quality European banks look attractive. ING is well positioned and its strength in deposit gathering is likely to be valued again.

Good write up with easy but I guess reasonable thesis.

Reg. gathering deposits: I think there is sth to it, ie stronger player in Germany and trusted brand I guess.

Further: ING has (one of) the top-notch cash pooling solution, incl. for FX accounts (non-EUR), as far as I understood comments from a large German enterprise.

Good read. I've had ING for a while now and I'm planning on keeping it. Given the past economic situation with extremely low interest rates. It's about to increase. Also the extra cash position of ING is something I value in a stock. As a ING user, I can vote for their good app and user experience.